Compound interest

Compound interest is the closest thing to a cheat code in personal finance, and it works just as brutally against you when you're in debt.

The context

Compound interest is trending because a new wave of financially curious people, largely Gen Z and millennials, are flooding search engines with basic-but-urgent money questions. Economic uncertainty, rising interest rates on both savings and credit cards, and a surge of personal finance content on social media have pushed the topic back into the spotlight.

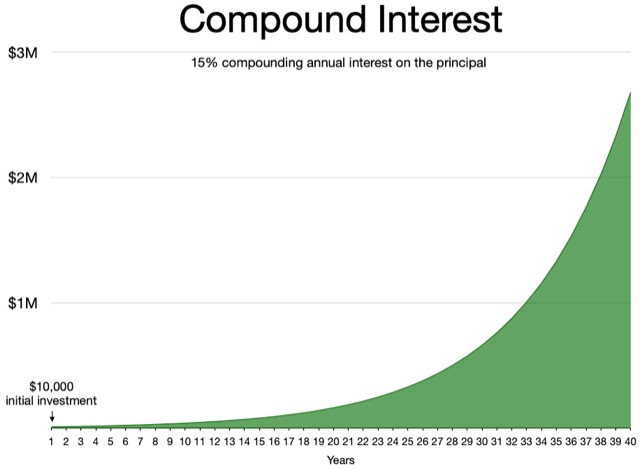

The concept is deceptively simple: you earn interest not just on what you put in, but on everything that’s already accumulated. That feedback loop is what makes it so powerful, and so dangerous depending on which side of it you’re on.

The Rule of 72 has become a viral shortcut in finance communities: divide 72 by your annual return rate to estimate how long it takes your money to double. At 7%, that’s roughly 10 years. It’s a back-of-the-napkin estimate, not a guarantee, but it makes the math feel real and urgent.

What’s driving urgency right now is the debt side of the equation. Credit card interest rates have climbed sharply in recent years, meaning compound interest is actively working against millions of borrowers. The same mechanic that builds wealth for patient investors is quietly draining people who carry high-interest balances month to month.

General information only, not personalized financial, tax, or investment advice. No return is guaranteed; all investing involves risk of loss. Any figures cited are illustrative or historical, not forecasts. Always cross-check with an official source or a qualified financial professional.